22 APRIL 2024

More than just a cherry blossom?

The beauty of the cherry blossom is breathtaking. You could admire them again this spring. Nevertheless, their short flowering period reminds us how fleeting the beautiful moments are.

Since mid-January, the stock markets have only known one direction. They have been rising, despite a multitude of state conflicts and wars, a gloomy economic outlook and stagnating corporate profits. The question therefore arises as to whether this bull market is like a cherry blossom – beautiful but short-lived – or whether there are other reasons besides a possible cut in key interest rates that speak in favor of equities in the long term.

Well, the first cracks have already appeared in the bull market. Contrary to the expectations of many market participants, the fight against inflation, particularly in the USA, is presenting the Fed with major problems. Unlike in the Eurozone, the first interest rate cut is likely to be a while in coming. This has caused share prices on Wall Street to crumble recently.

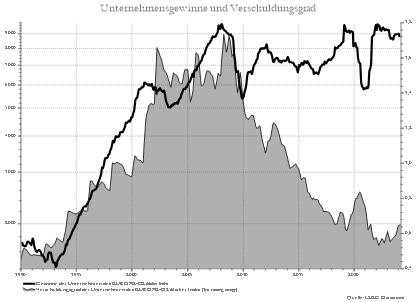

Debt-equity ratio has fallen sharply

Are there other reasons for prices to continue rising? Yes! Because: although corporate profits have stagnated in real terms for more than 15 years, it is clear that the quality of companies‘ balance sheets has improved significantly, as the level of debt has fallen significantly.

Funding of expansion investments drove the sharp rise in profits from the mid-1990s to 2008. As a result, companies massively increased their debt. The 2008 financial crisis changed the earnings outlook and many companies came close to insolvency due to their high debts. Such a situation should never arise again. Well, the companies have kept their word. Since then, companies used their profits to pay off debt rather than for expansion investments or for paying their shareholders.

Sound balance sheets benefit shareholders

The reporting season for 2023 therefore came as a surprise not because of the corporate profits, but because of the dividend announcements. Due to the solidity of the balance sheets, this makes sense also in retrospect. After 15 years of paying down debt, companies can now use profits for expansion investments or for their shareholders.

The Contrarian Value Euroland fund has also benefited from this. In our investment approach, which has been tried and tested for more than 25 years, we look for undervalued companies with comprehensible business potential. In doing so, we invest like an entrepreneur looking for business opportunities, even if this means swimming against the prevailing market current. This is why the fund has benefitted from the latest developments.

Of course, this does not mean that the positive trend on the stock markets will continue without setbacks, as seen in recent price falls. However, there are certainly good reasons to invest in stocks. Rising stock prices do not necessarily have to be just a cherry blossom.

Translation for convenience only!

About the author: Hans Peter Schupp is a managing partner of Fidecum AG und the portfolio manager of the Contrarian Value Euroland Fund.